The Research

Why the wealthiest families pay almost nothing in taxes — and how the same tools are available to everyone who learns to use them.

From Law School to a Billion-Dollar Mission

After working across virtually every legal niche — business formation, estate planning, tax strategy, immigration, contracts, intellectual property — one pattern became impossible to ignore: the wealthiest families and corporations consistently paid a fraction of what everyone else paid in taxes, not through evasion, but through structure.

The tools exist in the tax code. They have existed for over 100 years. The problem is not access — it is awareness. Attorneys, accountants, and financial advisors operate in silos. Estate planning happens without tax strategy. Tax strategy happens without charitable planning. Charitable planning happens without investment structure. The lack of coordination creates massive, preventable leaks — wealth that disappears into probate courts, estate taxes, and capital gains that could have been redirected entirely.

Two law degrees. Tens of thousands of hours studying the intersection of tax law, nonprofit structure, estate planning, charitable investing, and philanthropic strategy. Studying billionaires. Studying foundations. Studying the code itself. What emerged is both infuriating and extraordinary — a clear, legal, IRS-approved pathway that virtually every business owner, investor, and family qualifies for, and almost none have been told about.

"The gap between what the wealthy pay and what everyone else pays is not luck. It is structure. And structure can be learned."

Most Americans Have No Plan. The Numbers Are Alarming.

Despite decades of estate planning awareness campaigns, the data from the 2025 Caring.com Wills Survey and federal mortality statistics reveals a crisis hiding in plain sight.

The 2025 Caring.com Wills Survey found that only 24% of Americans have a will — down from 33% in 2022. The most common reason: it's "low on the to-do list." The result is that approximately 2.6 million probate cases are filed every year, consuming court time, legal fees, and family wealth that could have been protected, redirected, or leveraged.

Estate planning, when it does exist, rarely incorporates strategic giving. The charitable tax deduction — available for over 100 years — remains the most underutilized tool in the American financial system. The ultra-wealthy use it as a cornerstone. Everyone else leaves it on the table.

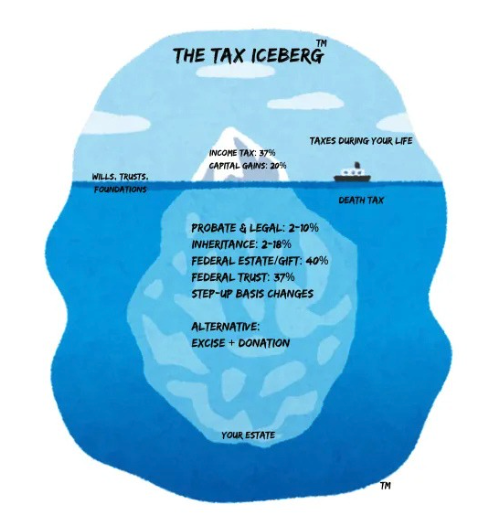

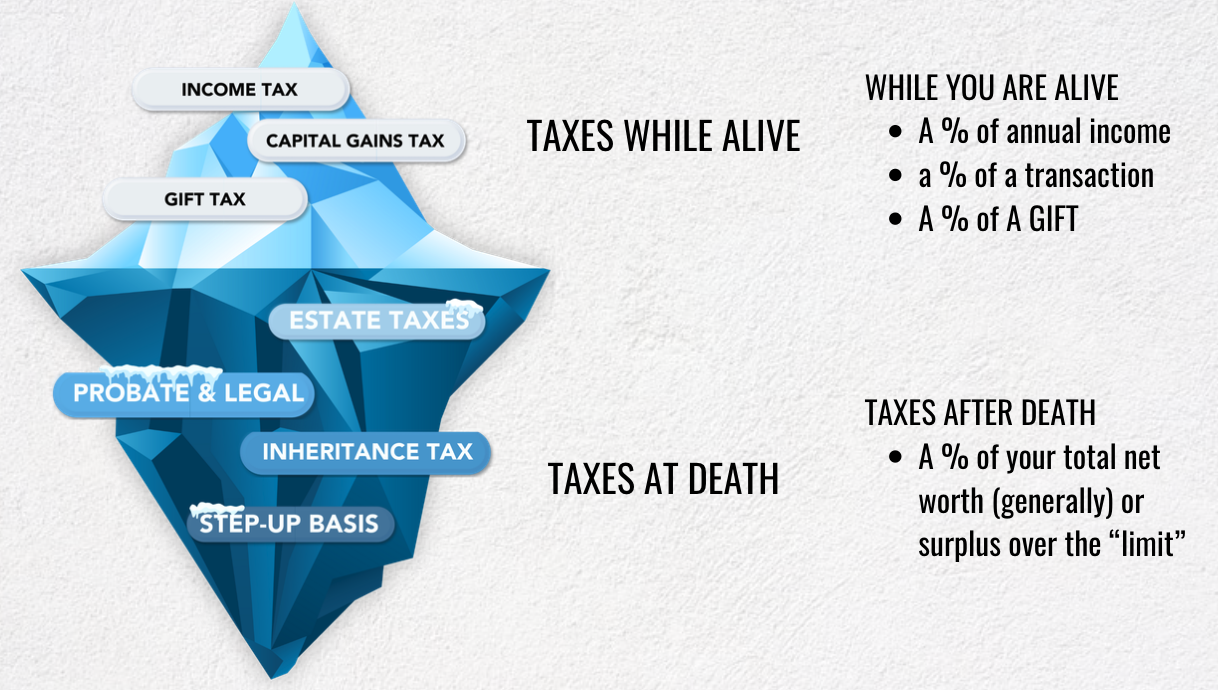

What You See Is Only the Beginning

Most people think of taxes as income tax and capital gains. But the full tax burden — the part below the waterline — is far larger and far more destructive to generational wealth.

Most of this can be planned for — but usually isn't. Strategic giving addresses taxes both while alive and at death, creating a comprehensive legacy plan that the ultra-wealthy have used for generations.

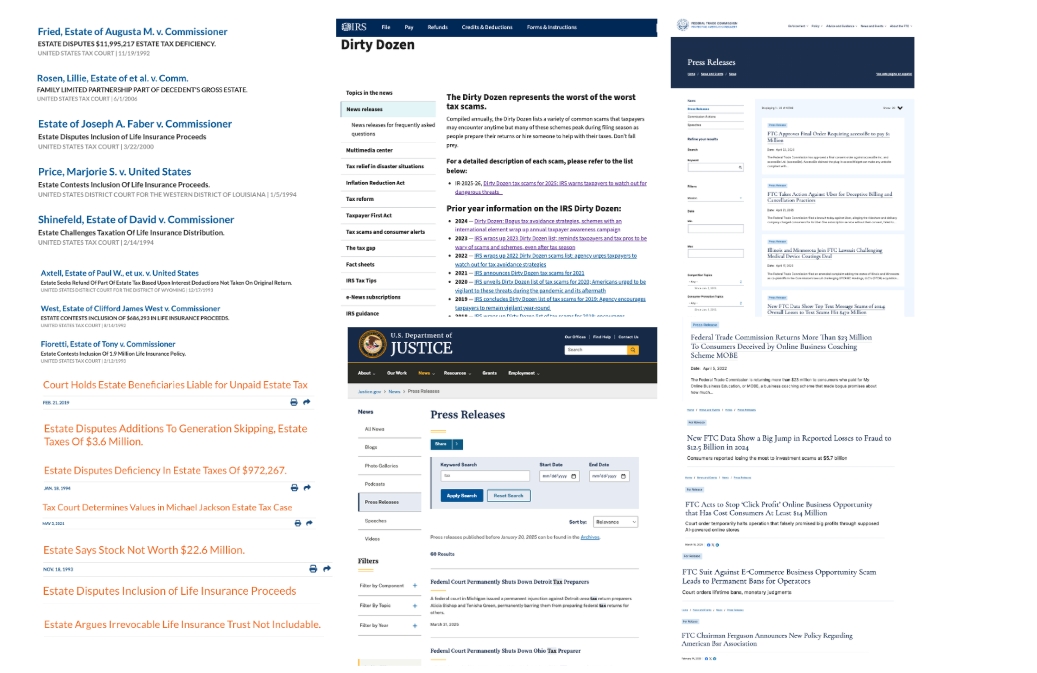

Too Many Scams. Too Little Coordination. Real Consequences.

As the charitable giving and tax strategy space has grown, so have the bad actors. The IRS publishes its annual "Dirty Dozen" — the worst tax scams targeting Americans. The DOJ and FTC have prosecuted hundreds of cases. The pattern is consistent: unguided, unstructured giving without proper legal and tax coordination creates massive vulnerability.

IRS Dirty Dozen + DOJ/FTC enforcement actions — the documented cost of unguided giving

The solution is not to avoid charitable giving — it is to do it properly. With the right legal structure, IRS-compliant documentation, and coordinated strategy, every dollar redirected is protected, deductible, and compounding. That is the difference between a scam and a strategy.

The Ultra-Wealthy Move Their Money Into Foundations and Nonprofits

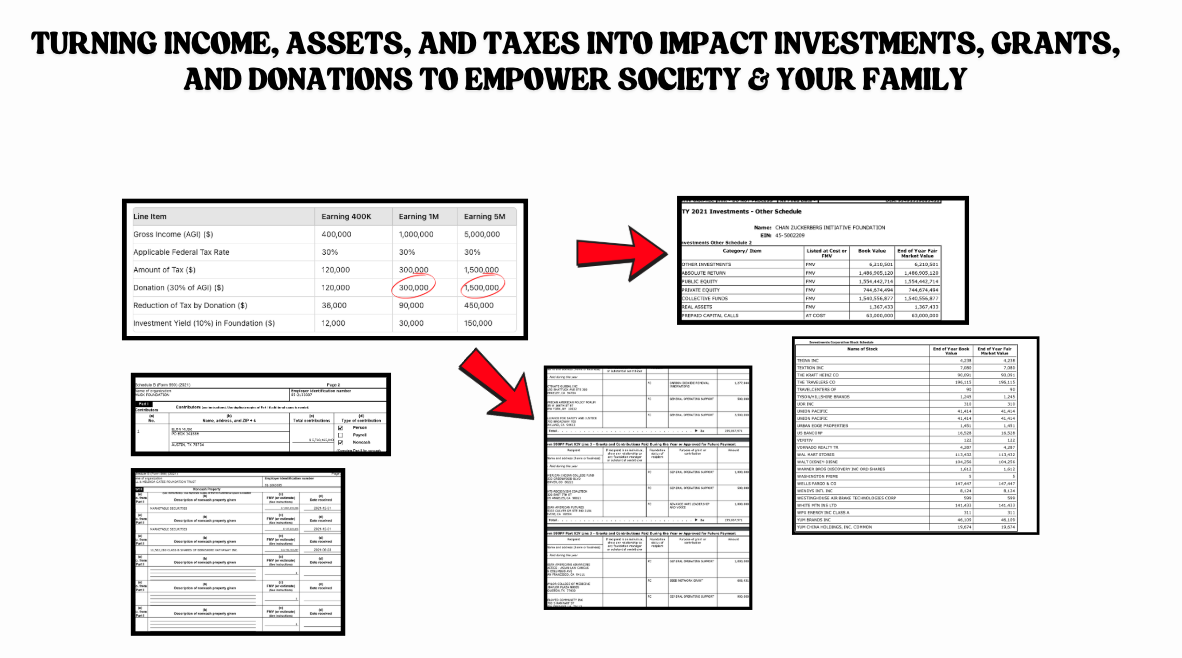

A consistent study of how the wealthiest families and corporations manage their wealth reveals one pattern above all others: they move significant portions of their income, assets, and appreciated investments into foundations and nonprofit structures — before taxes are triggered.

The math is not complicated — it is just not taught. A donor earning $500,000 who structures a $100,000 donation into a private foundation reduces their effective tax burden by 20–60%, retains investment control over the donated assets, and builds a multi-generational legacy vehicle. The same income. The same tax dollars. Redirected in a different way.

Income → Giving → Taxes → Investing → Legacy

The current model puts giving last. The strategic model puts giving first — and everything changes. This is not a loophole. It is the law, designed to fund society directly.

| Line Item | Earning $400K | Earning $1M | Earning $5M |

|---|---|---|---|

| Gross Income (AGI) | $400,000 | $1,000,000 | $5,000,000 |

| Federal Tax Rate | 30% | 30% | 30% |

| Amount of Tax | $120,000 | $300,000 | $1,500,000 |

| Donation (30% of AGI) | $120,000 | $300,000 | $1,500,000 |

| Reduction of Tax by Donation | $38,000 | $90,000 | $450,000 |

| Investment Yield (10%) in Foundation | $12,000 | $30,000 | $150,000 |

Hundreds of Federal Estate Tax Cases — The Cost of No Plan

These are not hypothetical scenarios. Federal estate tax court cases — from $972K to $11.9M in disputed taxes — document the real, documented cost of unplanned estates. Every one of these cases represents a family that could have structured differently.

The pattern across these cases is consistent: estates that lacked coordinated legal, tax, and charitable structure faced disputes ranging from hundreds of thousands to tens of millions of dollars. The attorneys, accountants, and advisors involved were not coordinating. Each was doing their job in isolation — and the families paid the price.

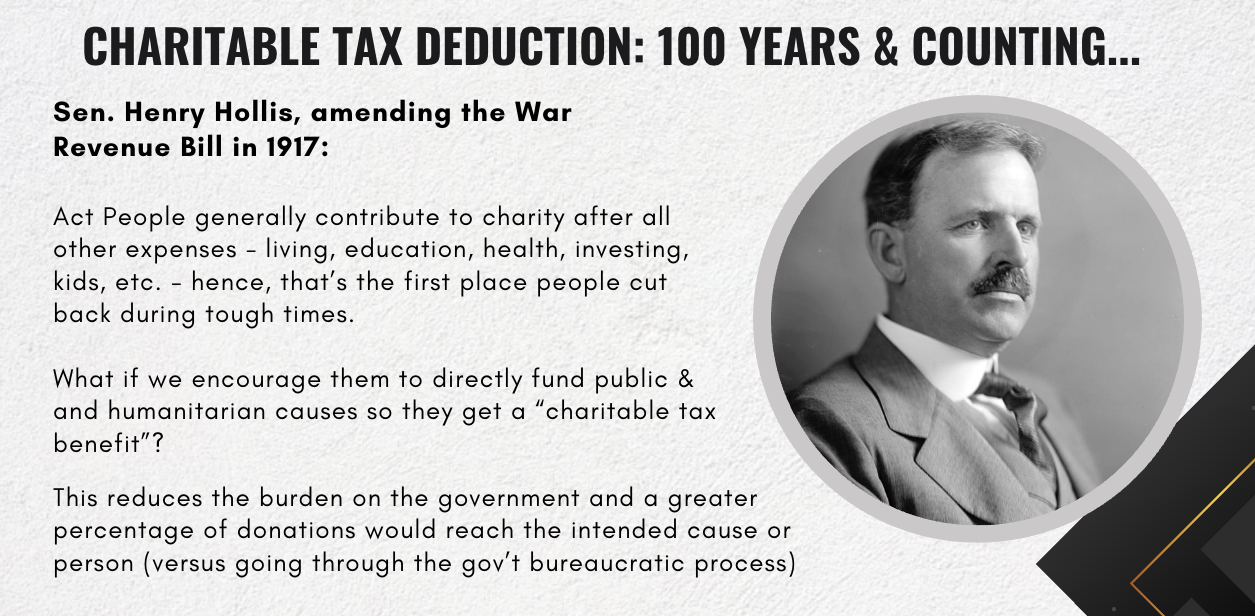

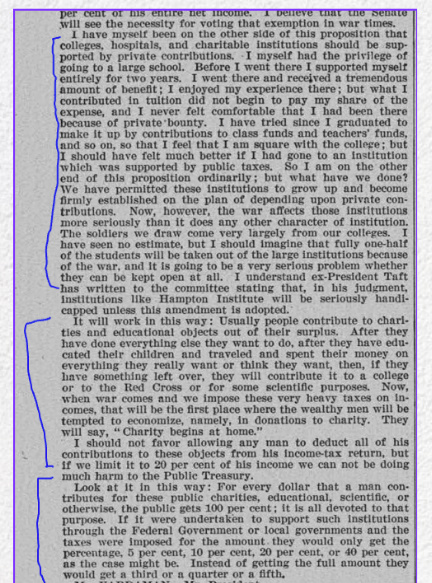

Charitable Tax Deduction: 100 Years & Counting

In 1917, Senator Henry Hollis amended the War Revenue Bill with a simple but profound observation: people contribute to charity after all other expenses — living, education, health, investing. It is the first thing cut during tough times. His solution was to incentivize giving before taxes, so that charitable causes could be funded directly rather than through government bureaucracy.

"For every dollar that a man contributes for these public charities, educational, scientific, or otherwise, the public gets 100 per cent; it is all devoted to that purpose. If it were undertaken to support such institutions through the Federal or local government, taxes would be imposed for the amount they would only get the percentage."

— Sen. Henry Hollis, 1917 Congressional Record

This is not a loophole. It is the original intent of the law. The charitable tax deduction has been in place for over 100 years, designed specifically to encourage individuals and businesses to fund public benefit activities directly — and to be rewarded for doing so.

Even in Scriptures — Every Tradition Teaches Strategic Generosity

The principle of strategic, intentional giving is not a modern tax strategy — it is a universal human principle embedded in every major faith tradition and philosophical framework.

Andrew Carnegie's "Gospel of Wealth" — published in 1889 — argued that wealth beyond personal need is a trust to be administered for the benefit of the community. He gave away 90% of his fortune. The tax code was designed, in part, to make this kind of intentional wealth redirection accessible to everyone — not just the ultra-wealthy.

The Tools Exist. The Law Supports It. The Only Missing Piece Is Coordination.

After 20 years, two law degrees, and 10,000+ cases across business, estate, tax, immigration, contracts, and intellectual property — the conclusion is clear: the lack of alignment and coordination between legal professionals is the single greatest cause of preventable wealth destruction in America.

The Billion Dollar Mission™ exists to close that gap — one foundation, one family, one organization at a time.

Ready to Apply the Research?

For nonprofits ready to 10x donor impact. For businesses exploring a nonprofit arm. For anyone who'd rather redirect their taxes toward something that matters. One conversation is all it takes.